Bousquet Holstein PLLC has appointed TAYLOR M. NUNEZ to the firm’s 2020 Summer Associate program. She is entering her final year as a candidate for a Juris Doctorate (JD) degree at Syracuse University College of Law and as a candidate for Master of Public Administration (MPA) degree at the Syracuse University Maxwell School of Citizenship […]

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

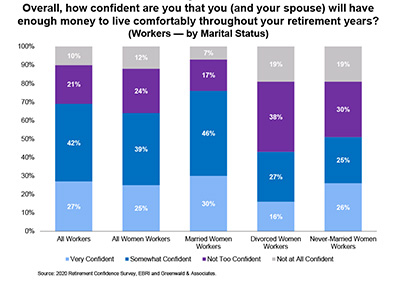

Survey: Unmarried women are less confident about their retirement prospects

Unmarried women had lower levels of retirement confidence than their married counterparts and were more likely to have fewer resources and be less prepared for retirement. That’s according to a new study that the Washington, D.C.–based Employee Benefit Research Institute (EBRI) conducted. The EBRI is a private, nonpartisan, nonprofit research institute based in Washington, D.C., that

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

How To Protect Retirement Savings In These Uncertain Times

The COVID-19 pandemic is causing millions of Americans to worry about their retirement savings and investments. Stocks are riding a roller coaster and the recent $2 trillion stimulus bill passed by Congress potentially means larger tax bills down the road to help pay for it. [Despite the recent strong rebound], the stock market could be

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

How To Retool Your Retirement Plan In The Midst Of COVID-19

The coronavirus pandemic has hit the economy hard, and people who are nearing retirement or already retired are feeling the stress. COVID-19 has caused a lot of retirees and those approaching retirement to rethink their plan for retirement. Falling interest rates, massive volatility in the stock market, and stifled economic growth are having a massive effect

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Owner of Buffalo accounting firm named NYSSCPA president

Edward L. Arcara, CPA, owner of Edward L. Arcara, CPA PC, which has three offices in Western New York, began his one-year term as board president of the New York State Society of CPAs (NYSSCPA) on June 1, the Society announced. He is the 101st president of the NYSSCPA, which was founded in 1897, and

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Tompkins Financial names tax, accounting expert to board of directors

ITHACA — Tompkins Financial Corp. announced it has recently added Ita M. Rahilly to its board of directors. She will continue as a director of Tompkins Financial’s affiliate, Tompkins Mahopac Bank, where she has served since 2018. Rahilly has served as a tax partner with the firm of RBT CPAs, LLP in Newburgh since January

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Broome County Council of Churches to use federal funding to build food market

BINGHAMTON, N.Y. — The Broome County Council of Churches will use $150,000 in federal funding for construction of a food market on the north side

Broome County playgrounds, courts, fields, and beaches reopen

BINGHAMTON, N.Y. — Broome County playgrounds, basketball courts, and athletics fields reopened on Friday, June 12, after County Executive Jason Garnar lifted an emergency order

Cazenovia College to start fall semester early so it can end by Thanksgiving

CAZENOVIA, N.Y. — Cazenovia College on Thursday announced that it’s planning for a fall 2020 academic calendar that will begin a week earlier with in-person

Destiny USA food and beverage tenants ask to be able to reopen in phase 3

SYRACUSE, N.Y. — A total of 41 food and beverage businesses at Destiny USA on Friday demanded New York State let them reopen under phase