Tech Farm II expansion at Cornell Agriculture and Food Technology Park in Geneva is complete

GENEVA, N.Y. — The expansion of the Cornell Agriculture and Food Technology Park Corporation’s (CAFTPC) Tech Farm II in Geneva is now complete. The project

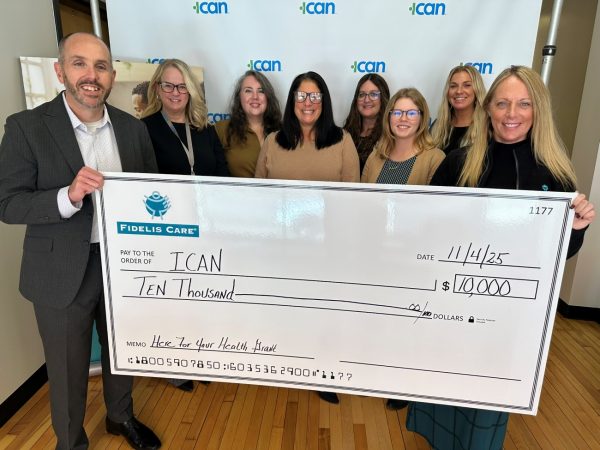

Fidelis Care awards $10K grant to Utica’s Integrated Community Alternatives Network

UTICA, N.Y. — Fidelis Care on Tuesday presented a $10,000 Here for Your Health maternal health grant to Integrated Community Alternatives Network (ICAN) in Utica. This grant is one of seven totaling $130,000 awarded to providers and community-based organizations that support innovative strategies in postpartum care and maternal mental health in underserved communities across New

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Clarkson CUHEAT program graduates first group of clean-energy trainees

POTSDAM, N.Y. — Clarkson University in Potsdam says the first participants in its Home Energy Awareness Training (CUHEAT) program have completed their training. The program

State approves merger of North Country credit union with AmeriCU

ROME, N.Y. — AmeriCU Credit Union tells CNYBJ that the New York State Department of Financial Services (DFS) has given final approval of its merger

Ithaca Area Economic Development names next president

ITHACA, N.Y. — Ithaca Area Economic Development (IAED) on Tuesday said it has selected the organization’s next president. Kurt Foreman — who has led the Delaware Prosperity Partnership (DPP) as president and CEO since 2018 — will join IAED in January 2026. Foreman assumes the role that Heather McDaniel previously held before she stepped down

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Upstate Golisano After Hours Care relocates to Nappi Wellness Institute

SYRACUSE, N.Y. — Upstate Golisano After Hours Care, a pediatric walk-in care center, has relocated from its Upstate Community Hospital location to the Nappi Wellness

Two Syracuse law firms to combine at the start of 2026

SYRACUSE, N.Y. — Two Syracuse law firms — Costello, Cooney & Fearon, PLLC and Scolaro Fetter Grizanti & McGough, P.C. — are combining to form Costello Cooney Fearon & Fetter, effective Jan. 1, 2026. “Costello Cooney Fearon & Fetter will build upon a combined 175 years of legal tradition in Syracuse while establishing a stronger

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

ALBANY, N.Y. — The new SUNY – NY Creates Technology Innovation Institute (TII) seeks to bolster future semiconductor research and workforce development. The institute will

State Police arrest two for thefts at Tractor Supply Cortlandville store

CORTLANDVILLE, N.Y. — New York State Police in Homer on Oct. 30 arrested two Syracuse women for stealing merchandise from the Tractor Supply store on State Route 13 in the town of Cortlandville. Nyraeisa Bibbs, age 27 of Syracuse, was charged with petit larceny, and Naughtica T. Fulton, age 23 of Syracuse, was charged with

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

NYPA issues first solicitations for new nuclear power project

ALBANY, N.Y. — The New York Power Authority (NYPA) on Thursday issued its first solicitations as part of a new initiative to develop 1 gigawatt