Otis Technology set for new leadership to begin 2026

LYONS FALLS, N.Y. — Otis Technology in Lewis County has promoted the company’s executive VP to serve as CEO, beginning Jan. 1, 2026. Brad McIntyre has worked for Otis for more than 25 years, per the firm’s Dec. 9 announcement. Otis Technology, which specializes in gun maintenance, is located at 6987 Laura St. in Lyons […]

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Griffiss Institute generated $15.4M impact on Mohawk Valley in FY24, study found

ROME, N.Y. — In fiscal year 2024 (FY24), Rome’s Griffiss Institute generated a more than $15 million impact on the economy of the Mohawk Valley.

Five Star Bank parent company completes $80 million subordinated debt offering

WARSAW, N.Y. — Financial Institutions, Inc. (NASDAQ: FISI), parent company of Five Star Bank, announced that it has recently completed a private placement of $80

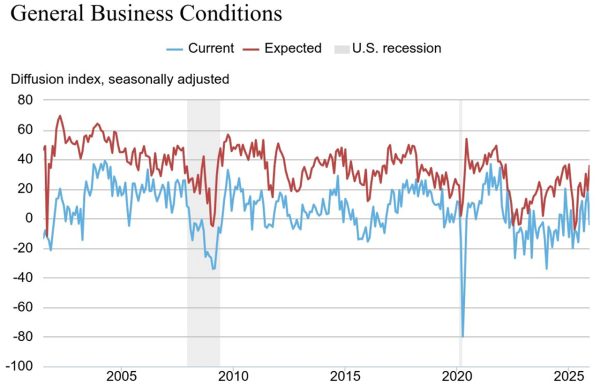

New York manufacturing index ends 2025 in negative territory

Respondents to the monthly Empire State Manufacturing Survey indicated unexpected contraction in the manufacturing sector with the general-business conditions index plunging 23 points to -3.9

Naturally Lewis Awards Night honors businesses, owners

LOWVILLE, N.Y. — A meat processor located northeast of Lowville is this year’s recipient of the Naturally Lewis Outstanding Business Award. Red Barn Meats, Inc. was among the businesses that Naturally Lewis recognized during its Membership Awards Night held on Nov. 19 at the Town Hall Theater in Lowville. The event brought together more than

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Riverside Farm Market formally opens at new location in St. Lawrence County

POTSDAM, N.Y. — Riverside Farm Market, a farm-direct store offering locally sourced products and prepared meals, recently formally opened at its new location at 6759 Route 11 in the town of Potsdam, in St. Lawrence County. The business, owned by Joe Eisele and Dean Laubscher, held a grand opening and ribbon-cutting ceremony with the St.

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Casullo appointed to M&T Bank Directors Advisory Council for CNY

SYRACUSE, N.Y. — M&T Bank recently announced it has appointed David Casullo, founder and CEO of Daneli Partners, to its Directors Advisory Council for Central New York. The 11-member council meets regularly to discuss business, customer, and community impact opportunities within Central New York and provides insights to support M&T’s ongoing efforts to develop locally

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

Oswego Hospital medical staff appoints new leadership

OSWEGO, N.Y. — The medical staff at Oswego Hospital recently appointed new leadership for 2025-2026, including David Bass, DO, as president and Michael Danise, MD, as VP, according to a Dec. 8 announcement from Oswego Health. Dr. Bass, a board-certified cardiologist, has served the community since 2020 through the Center of Cardiology at Oswego Health

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

New York cheese production rises more than 4 percent in October

New York production facilities produced nearly 78 million pounds of cheese (excluding cottage cheese) in October of this year. That’s up 4.2 percent from the approximately 74.8 million pounds produced in both September 2025 and October 2024, the USDA’s National Agricultural Statistics Service (NASS) recently reported. U.S. cheese production (excluding cottage cheese) totaled about 1.26

Get Instant Access to This Article

Become a Central New York Business Journal subscriber and get immediate access to all of our subscriber-only content and much more.

CNYSME selects Benz as the 49th recipient of its Crystal Ball Award

SYRACUSE, N.Y. — A Syracuse real-estate developer will be the 49th recipient of the Crystal Ball Award from the Central New York Sales & Marketing